If you’re planning on building a home there are a number of costs you’ll have to pay out of pocket before breaking ground. Here are a few things to be prepared to pay for before your construction loan is set up:

Costs related to design, engineering, permits, and loan closing are the primary expenses you’ll incur before you break ground building your house. Depending on market conditions when you build, you may also need to place deposits on long lead items like trusses or windows.

Most of us who endeavor to build a house, either with a contractor or on our own, will rely on a construction loan to finance the project. In this article, we’ll breakdown some of the costs you’re likely to incur during the planning and initiation phases of your project.

Costs Before You Break Ground

When I was preparing to build my house, I quickly became aware of some major expenses I would have to pay for out of pocket before I could start a construction loan. It was important to budget for these costs to be sure I had enough to pay the closing fees on the construction loan to get the whole process started.

In preparing this article, I am assuming that you already own a lot and are developing a house plan specific to that lot. If you haven’t bought a lot, add that cost in too.

Once we purchased our lot, we got to work putting our floor plan together. Though I’ve never worked as a drafter, I tutored the drafting class during my undergraduate. So I used that experience and drafted our floor plan myself. As I neared completion, I had to decided whether to hire an engineer to review the plans.

When the plans were completed and engineered, we decided to get our building permit before we closed on our construction loan. With the permit in hand, we were ready to close on our construction loan and start the clock on building our custom home (our lender requires construction be completed within one year of closing).

Design

A good set of house plans is critical to building a custom home. Depending on how you procure your plans, the price you will pay varies. Premade house plans can be bought from online vendors. You could hire a drafter or an architect to make a fully custom set of plans. Or, if you have the skill set, you could draft the plans yourself.

A simple google search for “house plans” will yield pages of results of vendors that have thousands of unique floor plans. Prices for these plans range from $1,100 for a set to $5,000 and up. Many of these sites allow freelance drafters to sell their unique floor plans. So be cautious before buying to ensure you’re getting a set of plans with sufficient details for your contractor to build. Or use these plans as a starting point, and hire a drafter to modify the floor plan that is just missing a few things you want.

If you can’t find the right plan for you, hiring an architect may be your best option. Architects are highly trained professionals that can do far more than just draw your plans. But their expertise comes with a price. Depending on the services rendered, architects will either charge a percentage of the total project (typically 8% to 15%) or a set price per square foot of the floor plan (typically in the $2 to $10 per square foot range).

They’ll provide insights into design considerations from everything to the orientation of the house on the lot to the size and depth of your closets. There are thousands of decisions to be made when making a custom floor plan, and an Architect can advise you along the way.

As mentioned previously, I chose to draft my own floor plan. Even with the skills I brought to the table (construction management background and proficiency in a drafting program), it took my wife and I months of design and review to work out all the details needed to get the floor plan we wanted.

The floor plan is foundation of your building process. Everything that happens during your build will reference this document. Take your time, and get the right floor plan. It’ll make all the difference.

Engineering

Depending on where you live and certain factors about your floor plan, you may be required to have an engineer review and approve your plans. If you live in a large municipality, you will almost certainly be required to have engineered plans.

Where I live, my county requires floor plans that have an open space greater than 900 square feet to be engineered. As this varies from place to place, you’ll have to call your local planning and zoning department to find out their requirements (typically detailed in the building permit application).

Even if not required, you may want to hire engineers for the benefit of their professional services. Building a house involves major risks, and engineers can help you reduce certain risks. I’ll briefly talk about three types you might consider; surveyors, geotechnical, and structural.

A surveyor ensures that you know exactly where your lot begins and ends. Building your house outside of the correct set backs in relation to your property boundary could be devastating to your project. For the services they provide, a surveyor will typically charge $400-$700.

Geotechnical engineers analyze the composition of the soil. They provide guidance that will ensure your house will be stable in the given soil conditions for your lot. Depending on your area, this can be critical. My cousin bought a house in a development that was built on blue clay. Due to the properties of that soil type, their house would creak and groan and the soil expanded and contracted throughout the year. A geotechnical engineer can help you mitigate risks like this. Their services require some physical services, like soil boring. Because of these services, a geotechnical report could costs $1000-$5000 dollars.

Finally, a structural engineer is likely the most common engineer used for residential house plans. Their services will size beams and headers, provide details for shear walls and tie-downs, and anything else needed to ensure your house is structurally sound. Even if not required in your location, you may consider hiring a structural engineer to review your custom floor plan. Where I live, structural engineers charge by the square foot of the floor plan ($0.25 to $2.00 per square foot). Some areas may charge by the hours or even just a percent of the construction costs.

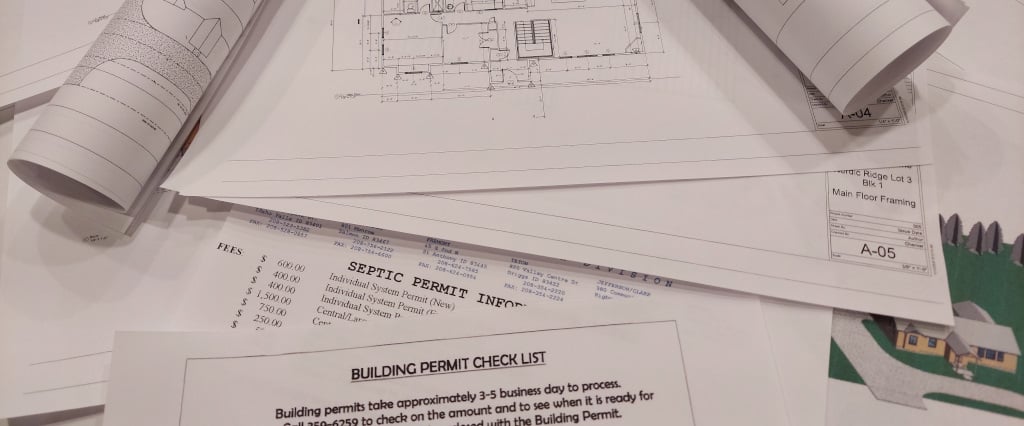

Permits

Depending on your project schedule, you may need to pay for your building permit before you close on your construction loan. Where I live, there multiple permits that need to be procured before I can even apply for my main building permit from the county. In all, you can expect to pay $2000 to $4000 in permit fees, depending on location and the size of your house.

The fee for the primary building permit is typically based on the square footage of your house. The municipality typically has a chart breaking down fees by a range. For example, the first range might be houses under 1500 SF. The second might be 1501 SF to 2500 SF. The larger your house, the more you’ll pay. This fee is used to pay for the building inspector that will sign off on certain milestones throughout your project.

As mentioned earlier, where I live the county requires a number of permits to be acquired before I can apply for the building permit. Because I live in a rural area, I need to have a septic permit. This too is based off the size of your house and can range from $300 to $500. I also need to acquire an Approved Driveway Access Permit from the county road and bridge department (approximately $50).

If you’re hiring a general contractor, you may not need to worry about these costs as they will be pulling the permits.

Closing

Depending on your circumstances, the down payment and closing costs could be the largest expenses you have before breaking ground on your house. Closing costs will typically be around 1-3% of your project costs (i.e. – on a $395K project, closing may costs around $4,500).

The larger costs could be the required down payment. Depending on the lender this could be 20% to 30% of the total project costs. If you own the lot, the lender will typically count this as equity toward the project, reducing the amount of cash you’ll have to provide as down payment.

For the purpose of this article, I am skimming the surface of the construction loan (mostly because this is an anticipated costs. The following article has more details regarding construction loan closing costs:

How to Get a Construction Loan

Long Lead Items

Depending on the market circumstances when you build your house, there may be materials or equipment that you’ll want to order before you break ground. At the time I’m writing this article, my local appliance store is saying the Kitchen Aid ranges are backlogged until 10 months. My building materials supplier is suggesting I order doors, windows, and trusses before I break ground. Someone I know just waited 6 months for their garage doors to arrive.

Many of these delays are due to the supply chain issues of 2020 and 2021. Nevertheless, when you build there could be other factors affecting the markets. Talk to local suppliers ahead of time, so you aren’t caught off guard by a long-lead time item that will delay your project.

Conslusion

Building a house can be throw a lot of curve balls that may catch you off guard. Now you know some of the curve balls that may come at you before you even get started.